Issue 05 · June 15, 2026

Brent at $87. The Reopening Is the Bearish Catalyst, Not the Relief Rally.

Brent fell to a three month low with Hormuz still shut. The reopening everyone fears is the bearish catalyst, not the relief rally.

This Week · The reopening as bearish catalyst · Russian crude revenue under the drones · Inventories at a 23 year low

Lead Story

Brent at $87. The Reopening Is the Bearish Catalyst, Not the Relief Rally.

Oil hit a three month low while the Strait of Hormuz is still shut. That is the proof that Chinese demand, not Gulf supply, now sets the price, and it flips the reopening from a spike into a slide toward the EIA's own $79.

Brent crude, the global oil price benchmark, settled at $87.33 a barrel on Friday 12 June, the lowest since early March and down about 7.7% on the week from $94.66. TTF, Europe's benchmark wholesale natural gas price, closed at €46.78 per megawatt hour, down about 3.5% on the week. Both fell for one reason: President Trump said a deal to reopen the Strait of Hormuz, the Gulf shipping chokepoint shut since late February, could be signed soon, and Qatari mediators flew to Tehran on 14 June to finalise a sixty day ceasefire extension that would lift the blockade and let Iran sell oil freely. The strait is still physically closed. Yet the price fell, because the news that mattered came from the demand side: China, the world's largest crude buyer, imported about 7.8 million barrels per day in May, an eight year low and roughly 33% below its 2025 average, as it leaned on refinery run cuts and inventory draws to absorb the loss of Gulf barrels.

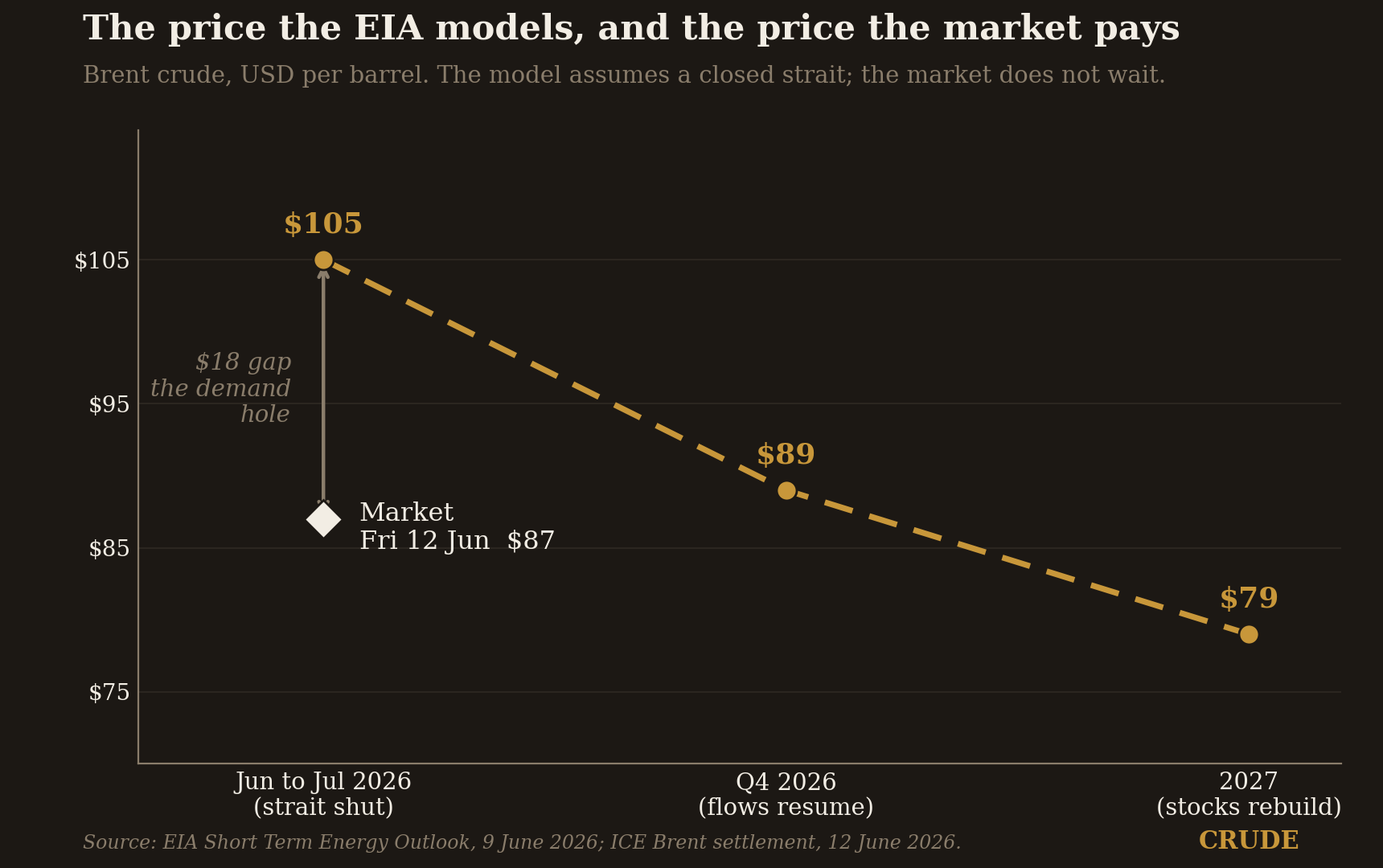

Here is the number that settles the argument. The EIA, the US Energy Information Administration that publishes the most watched oil data, said in its June outlook that Brent should average $105 a barrel in June and July on the assumption the strait stays closed. The screen says $87. That $18 gap is a Chinese demand hole no supply model can see. For three issues Crude has argued that demand, not the Gulf, sets the oil price, and a three month low printed while the chokepoint is still shut, on nothing more than a deal rumour, ends the debate. The read for a European investor over the next 30 to 90 days inverts the conventional trade. The reopening everyone is bracing for as a relief is the opposite for oil: it removes the last thing holding Brent up. When Iranian and idled Gulf barrels return into a market that has lost more than 3 million barrels per day of Chinese buying, they will not spike the price, they will accelerate the slide toward the $79 average the EIA already forecasts for 2027. For a European driver that means cheaper fuel ahead rather than a shock; for anyone holding oil linked positions, the signature is the sell signal, not the rally.

Chart · EIA Brent forecast versus the screen

The EIA still models Brent at $105 a barrel for June and July on a closed strait, easing to $89 by the fourth quarter and $79 across 2027 once flows resume. The market is already trading near $87 with the strait shut. The gap between the supply model and the screen is the Chinese demand collapse the forecast cannot price, and it points the same way the EIA's own 2027 number does: down. (EIA Short Term Energy Outlook, 9 June 2026)

The reopening everyone is bracing for as a relief is the opposite for oil: it removes the last thing holding Brent up.

Geopolitics

The Reopening That Drains Moscow's War Chest

A Brent crash does to Russian oil revenue what three years of price caps could not, just as Ukraine's drones cut the volume Russia can ship.

The deal that would reopen Hormuz also lets Iran sell oil freely again, and the resulting flood of returning barrels lands on a Russia already losing export capacity to Ukraine's drone campaign. Ukrainian strikes forced central Russian refineries at Ryazan, Moscow, Kirishi, Nizhny Novgorod and Yaroslavl to halt or cut output through May, driving a 24% month on month drop in seaborne crude exports after the April raids and a 65% year on year fall in oil product exports between January and April; Moscow has banned gasoline exports until 31 July, and its crude export revenue fell 9% month on month to €374 million per day in April. For Central and Eastern Europe the reopening is a double edged relief. Cheaper oil eases the fuel and inflation pressure the region has carried since February, and a Brent slide toward the EIA's $79 collapses Russian per barrel revenue exactly as the drones cut the barrels Russia can move, a squeeze on the war economy that sanctions never delivered. The catch is that the same low price weakens the economic case for the costly diversification away from Russian crude and gas, the Gdansk reroute and the LNG cargoes documented in earlier issues, and risks a quiet relapse into dependence the moment the emergency passes. Austria and Germany, carrying the deepest exposure, would feel that pull first.

In Focus · Inventories

Stocks at a 23 Year Low, and the Price Still Fell

The deficit is real and historic. Demand is winning anyway.

The underappreciated number in the EIA's June outlook is not the price forecast, it is the inventory one. OECD commercial oil stocks are set to fall to about 50 days of demand cover by the end of 2026, the fewest since January 2003, after Middle East producers cut output by more than 11 million barrels per day and global inventories drew an average 6.3 million barrels per day in the second quarter. In the United States, crude stocks fell another 7.2 million barrels in the week to 5 June, to about 5% below the five year average, while distillate stocks, the diesel, heating oil and jet fuel category, sit roughly 13% below their five year norm, deeper than the 11% gap of late May. This is the cleanest proof yet of the argument that has run through Crude since issue one. A 23 year low in inventories is the textbook setup for prices to rise, and Brent instead hit a three month low. When demand falls faster than supply, even multi decade thin stocks cannot lift the price. The structural deficit that opened the Crude story has lost, on the screen, to the demand collapse, and the European consequence is concrete: the relief in fuel costs is coming, but it arrives because consumption broke, not because supply healed.

Take Action

Five Signals to Watch This Week

Concrete checkpoints between now and the next issue.

- Read the IEA Oil Market Report due 17 June at iea.org. The Paris based International Energy Agency releases the first report to fully capture the Hormuz era demand collapse; a deeper demand cut is bearish for oil even if the strait reopens.

- Treat the Hormuz signature as a sell signal, not a relief rally. Qatari mediators have been in Tehran since 14 June; if the memorandum signs, expect oil linked positions to slide toward the EIA's $79 path for 2027 rather than spike.

- Watch China's June crude customs print in mid July. May hit an eight year low of 7.8 million barrels per day; a rebound is the one thing that lifts the price, continued weakness confirms the demand cap.

- Set Brent alerts at $89 and $79. The EIA's Q4 2026 target of $89 is already breached at $87; the next marker is the EIA's $79 average for 2027, and a reopening closes that gap fast.

- Check Russia exposure in anything you hold. A price crash from a reopening cuts Moscow's per barrel revenue, already down 9% to €374 million per day in April, just as Ukrainian drones cut export volume; cheaper oil helps European consumers but risks stalling the shift away from Russian supply.