Issue 02 · May 25, 2026

Oil Is Near $104. The Demand to Justify It Is Already Gone.

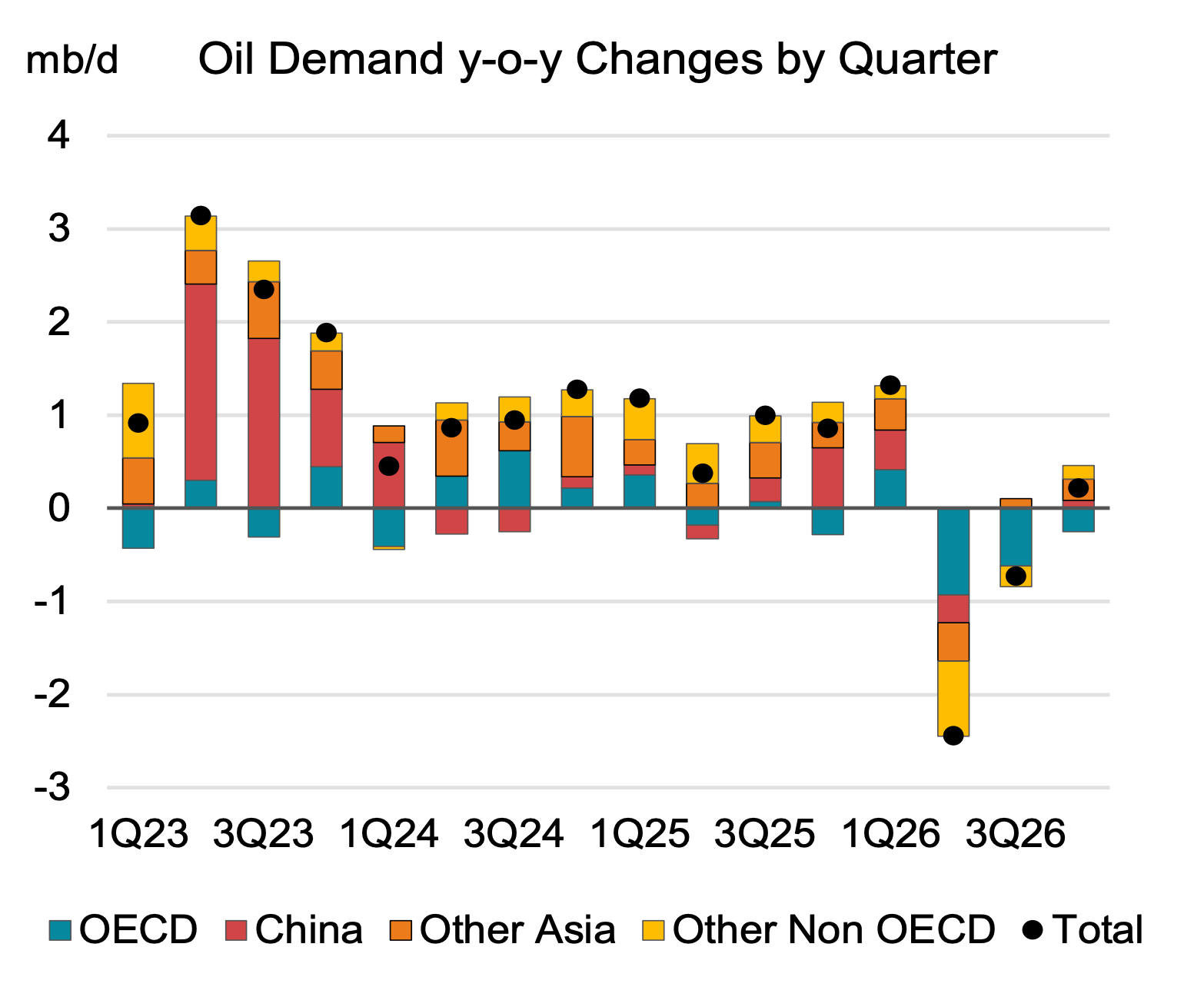

The supply shock has a shorter shelf life. Demand was already falling before Hormuz reopens.

Lead Story

The Supply Shock Has a Shorter Shelf Life

Demand was already falling

Brent crude settled at $103.94 per barrel on the Friday 22 May 2026 close, a weekly decline of approximately 3.7%. TTF, Europe's benchmark wholesale natural gas price, closed at €48.69 per megawatt-hour on 22 May 2026, down roughly 2.6% on the week. Both moves reflected ongoing pressure on demand as the Strait of Hormuz closure continued to suppress consumption.

After markets closed on Friday, Trump claimed on 23 May that a deal to reopen the Strait of Hormuz is "largely negotiated," which Iran's semi-official Fars news agency immediately dismissed as "incomplete and inconsistent with reality."

The International Energy Agency projects global oil demand will contract by 420,000 barrels per day in 2026 compared to 2025, the first annual decline since COVID-19. The US Energy Information Administration puts Brent at $89 per barrel in Q4 2026 as Middle East production gradually recovers.

When Hormuz reopens, that additional supply lands in a market where demand has already broken.

For a European retail investor holding oil-linked assets, the supply shock premium has an expiry date: watch for any confirmed Hormuz reopening announcement as the trigger for a repricing of oil-linked positions downward over the following 30 to 60 days.

Geopolitics

Berlin's Fuel Supply Exposed by Druzhba Halt

The pipeline pressure point shifts

On 1 May 2026, Russia halted Kazakh crude transit through the northern branch of the Druzhba pipeline (the Soviet-era pipeline network that has historically supplied eastern Germany's refineries) to the PCK Schwedt refinery in northeastern Germany. PCK Schwedt provides roughly 90% of fuel to the Berlin and Brandenburg region and feeds jet fuel to Berlin Brandenburg Airport (BER).

The suspended Kazakh flows represented approximately 17% of the refinery's annual crude supply, or around 43,000 barrels per day. Germany is now routing replacement crude through the Polish port of Gdansk via PERN, Poland's pipeline operator. Every barrel moved through Gdansk carries a higher cost than Druzhba delivery.

For Berlin, this is not an abstract supply security concern: it translates directly into fuel margins at the pump and jet fuel costs for every flight out of Berlin Brandenburg Airport (BER).

In Focus: Refining

Global Refinery Output Falls to COVID-Era Lows

American margins widen, European feedstock vanishes

The IEA projects global refinery throughputs (the total volume of crude oil used as raw material input by refineries worldwide) will plunge by 4.5 million barrels per day in Q2 2026 to 78.7 million barrels per day, the sharpest quarterly reduction since the pandemic.

American refiners are running at 91.6% of their maximum operable processing capacity as of the week ending 15 May 2026 (EIA), absorbing high margins while European and Asian operators cannot source the crude oil they need to match that rate. US refiners, protected by domestic crude supply from the Gulf of Mexico and shale basins, are capturing the refining profit that European operators cannot reach.

That margin gap between American and European refiners widens with every week the Strait of Hormuz remains closed, and the cost falls on European consumers through diesel and jet fuel prices.

Commodities

Europe Is Absent From the Critical Minerals Chain

90% of flows go east

According to Blanca Navarro Boza, Traffic Responsible at Altamira Trade AG, the commodity that will define the next phase of industrial development is not copper but rare earths, a group of 17 metals essential for electric motors, wind turbines, electric vehicle batteries, and military guidance systems.

China controls the overwhelming majority of global rare earth processing. Europe, Navarro Boza confirms, receives no critical mineral concentrate flows from her firm's South American and African operations. She connects the Trump-Zelensky minerals agreement directly to a US strategic move to secure Ukraine's critical mineral deposits before others can.

For a European retail investor, the exposure is structural: every wind turbine and electric vehicle motor assembled in Europe depends on a supply chain that currently runs entirely through Beijing.

Source: Blanca Navarro Boza, Traffic Responsible, Altamira Trade AG.